In May 2026, the Indian banking landscape is witnessing a tectonic shift. For decades, Public Sector Banks (PSBs) were synonymous with safe but static Fixed Deposits (FDs). However, as we move through 2026, the narrative is changing. PSBs like State Bank of India (SBI) and Indian Bank are no longer content being just repositories of savings; they are aggressively pivoting toward the lucrative world of wealth management.

This “Great Shift” is driven by a maturing Indian investor who is increasingly looking beyond traditional savings vehicles in search of higher inflation-adjusted returns. With India’s BFSI sector boasting its cleanest balance sheets in a decade, the timing for this expansion couldn’t be better.

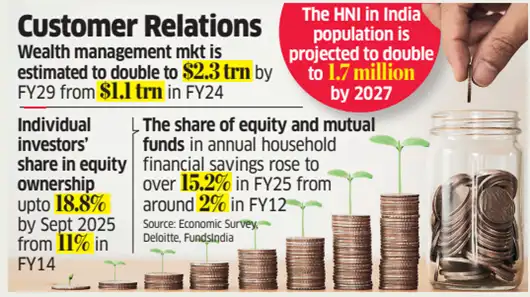

The Numbers Behind the Boom: India’s Growing HNI Population

The scale of the opportunity is staggering. Recent data suggests that India’s High Net Worth Individual (HNI) population is projected to double to 1.7 million by 2027. This surge in private wealth is not limited to Tier-1 metros; significant wealth creation is happening in Tier-2 and Tier-3 cities, exactly where PSBs have their deepest roots.

According to industry estimates, the Indian wealth management market is set to double to $2.3 trillion by FY29. For PSBs, this represents a massive untapped revenue stream that can supplement their core lending business with high-margin fee income.

PSBs Leading the Charge: SBI and Indian Bank’s Strategic Pivot

Leading the pack, the State Bank of India has significantly expanded its ‘SBI Exclusif’ offering, targeting the mass-affluent and HNI segments with personalized investment solutions. Similarly, Indian Bank has been vocal about its intentions to build a dedicated wealth management vertical, leveraging its vast branch network to reach customers who were previously ignored by private wealth firms.

This move is also a defensive strategy. As fintech consolidation continues to reshape the market, PSBs are realizing that they must offer sophisticated financial products to retain their core deposit base. By integrating agentic AI in banking, these institutions are now able to provide high-quality advisory services at scale, bridging the gap between traditional banking and modern portfolio management.

From Savings to Solutions: Why Wealth Management is the New Frontier

The transition from a “savings first” to a “solutions first” mindset is evident in the product suites being rolled out. PSBs are now offering everything from curated mutual fund portfolios and Portfolio Management Services (PMS) to Alternative Investment Funds (AIFs) and insurance-linked investment products. The recent RBI credit card reforms have also played a role, as banks look to cross-sell wealth products to their premium cardholders.

Challenges and the Path Ahead: Technology vs. Trust

While the opportunity is vast, the road is not without hurdles. PSBs face stiff competition from established private players and nimble fintech startups. The success of their wealth management betting will depend on two factors: technology and trust. While PSBs already enjoy immense trust among the Indian masses, they must rapidly upgrade their digital interfaces to match the seamless experience offered by private competitors.

As we look toward 2027 and beyond, the democratization of wealth management through PSBs could be the single most important factor in the financialization of Indian household savings. The “Great Shift” is well underway, and the winners will be those who can blend the traditional trust of a public institution with the modern efficiency of a tech-driven wealth advisor.